Guaranteed Annual Grants

Tax-Free Growth

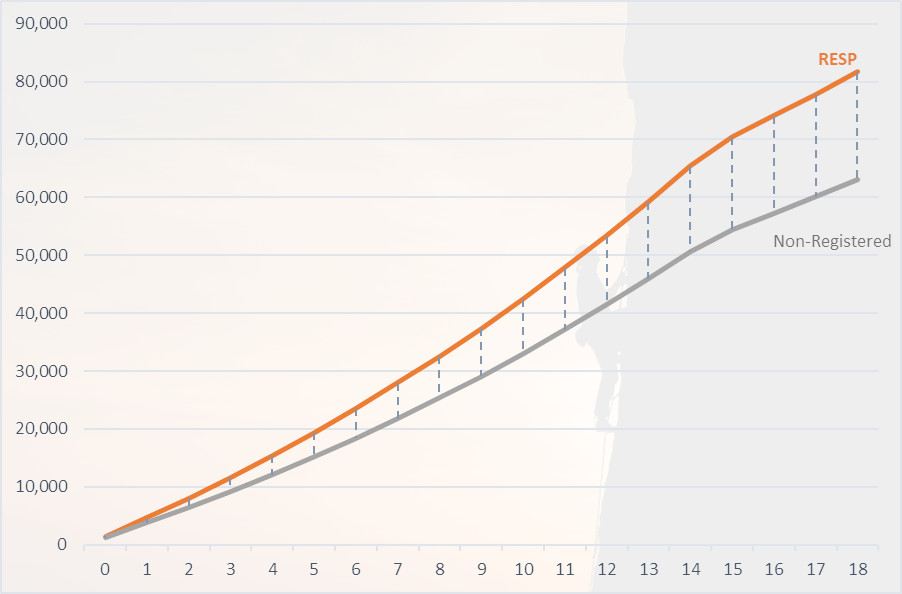

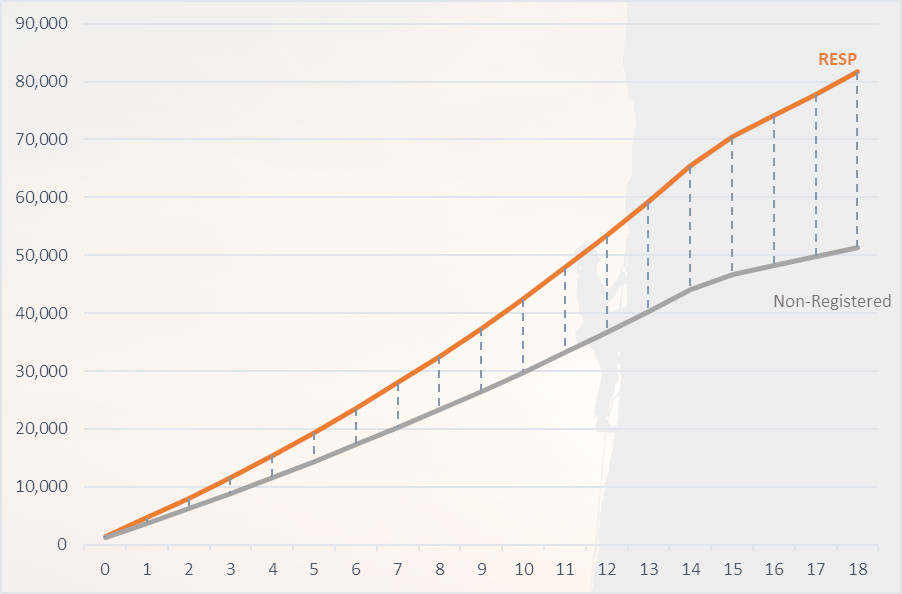

RESP vs Non-Registered savings

RESP vs Non-Registered Savings

For illustration purposes only

-

Contributing $200 per month from age 6 months to age 14.5

-

Matching federal and QC grants

-

5% interest income

No tax

53.31% marginal tax rate

Close

Anyone can contribute

Grandparents, extended family, close friends, and anyone else willing to support can give towards the RESP.

Flexible savings

Tax-advantaged withdrawals

When withdrawn for enrolment in a qualifying post-secondary educational program, plan growth, and government grants will be taxed at the student’s tax rate. Withdrawal of contributions is always tax-free.